Smart, predictive lending is going mainstream in 2025. See how AI spots your cash gap early, what that means for credit, and what changes in 2026.

The new reality: loans arrive before the panic

A strange moment is becoming normal.

You feel fine. You are not searching for a loan. You are not even thinking about debt. Then your bank app, payroll app, or merchant dashboard flashes a “pre-approved” offer. It feels timely. It feels almost psychic. It also feels dangerously easy.

This is the rise of smart loans, a transformative idea in modern credit. Instead of waiting for you to ask, AI tries to predict when you will need capital. It watches signals. It forecasts stress. It then pushes a verified offer at the exact moment you are most likely to accept.

Consequently, borrowing becomes proactive. It becomes embedded. It becomes deeply personal.

However, this is not a cute convenience feature. It is a critical shift in power. It changes who controls timing. It changes who frames the story. It changes what “responsible lending” even means in 2025.

Why this feels like a breakthrough

Traditional credit is reactive.

A borrower hits a tight spot. They apply. They explain. They wait. The lender checks history. The lender decides. The money arrives late, or never.

Smart loans flip that timeline. A model anticipates the tight spot. A system prepares an offer. A decision is instant. Funding can be immediate.

That speed can be rewarding. It can prevent late fees. It can protect a credit record. It can reduce stress.

Additionally, for small businesses, this can be life-saving. A sudden inventory gap can kill momentum. A fast working-capital line can keep a company thriving.

Still, the same speed can create reckless borrowing. It can also create silent manipulation.

The big question of 2025

The central question is simple.

If AI knows you are vulnerable before you do, will it help you or exploit you?

In 2025, both outcomes are possible. The difference is design. The difference is governance. The difference is trust.

What a “smart loan” really is

A smart loan is not one product.

It is a lending system that uses predictive analytics and machine learning to estimate a future need for capital. Then it delivers an offer early, sometimes days or weeks ahead of the moment you would normally apply.

Furthermore, smart loans often sit inside products you already use. This is part of embedded finance. The lender may be a bank. The interface may be a platform. The money may come from another balance sheet entirely.

That mix is powerful. It is also confusing.

The prediction engine: signals, forecasts, and risk

Smart-loan models typically look for patterns like these:

- Incoming cash patterns, like salary deposits or sales revenue

- Spending spikes, like seasonal inventory or tuition payments

- Volatility, like irregular income or unstable expenses

- Early stress signals, like overdrafts or shrinking cash buffers

- Repayment behavior, like consistent bill timing

The most important category is cash flow data.

Cash flow is emotional because it is real. It reflects your daily life. It also creates a seductive feeling of certainty.

Yet cash flow is not perfect. It can be messy. It can be misread. That is why responsible lenders focus on strong variables and tight controls, not raw surveillance.

Research and industry reporting in 2025 increasingly highlight cash-flow underwriting as a serious tool for smarter credit decisions. (FinRegLab)

The delivery layer: proactive offers inside your life

Prediction is only half the story.

The other half is delivery. Smart loans are delivered where you already are:

- A bank app offers a line increase before a bill storm

- A payroll app offers early wage access or a small loan before payday

- A marketplace offers working capital before your stock runs low

- An invoicing tool offers a loan when receivables slow down

Consequently, the loan becomes a product feature, not a separate financial journey.

That is the invisible part. It feels safe because it feels familiar.

Why this exploded in 2024 and 2025

Smart loans did not appear from nowhere.

They rose because three forces collided: data access, automation, and competitive capital.

Open finance makes prediction easier

Open banking and open finance frameworks make it easier to access verified financial data with user permission. That data can improve risk models and forecasting.

The World Bank has discussed how open frameworks can enable access to financial data with strong predictive value, while also stressing the need for safeguards. (World Bank)

Additionally, fintech infrastructure has matured. APIs and permissioned data flows have become more standardized. That reduces friction. It also raises privacy stakes.

GenAI and automation shrink decision time

Automation has attacked the slow parts of credit.

Document intake is faster. Fraud screening is sharper. Loan origination workflows are increasingly automated. GenAI is also being explored for tasks across the credit lifecycle, from analysis to communications.

McKinsey has discussed how genAI can support parts of the credit business and accelerate work in credit processes. (McKinsey & Company)

Consequently, lenders can act earlier. They can also act at scale.

Competition and private credit push growth

In 2025, private credit firms have expanded aggressively into consumer-related debt exposure, increasing competitive pressure and changing funding dynamics. (Financial Times)

When capital wants yield, lenders want volume. When lenders want volume, proactive offers become tempting.

However, volume without discipline is fragile. That is why 2025 also brings louder warnings about underwriting quality and model risk.

How AI predicts your need for capital

This is where the story gets fascinating.

Prediction is not magic. It is pattern recognition with a feedback loop.

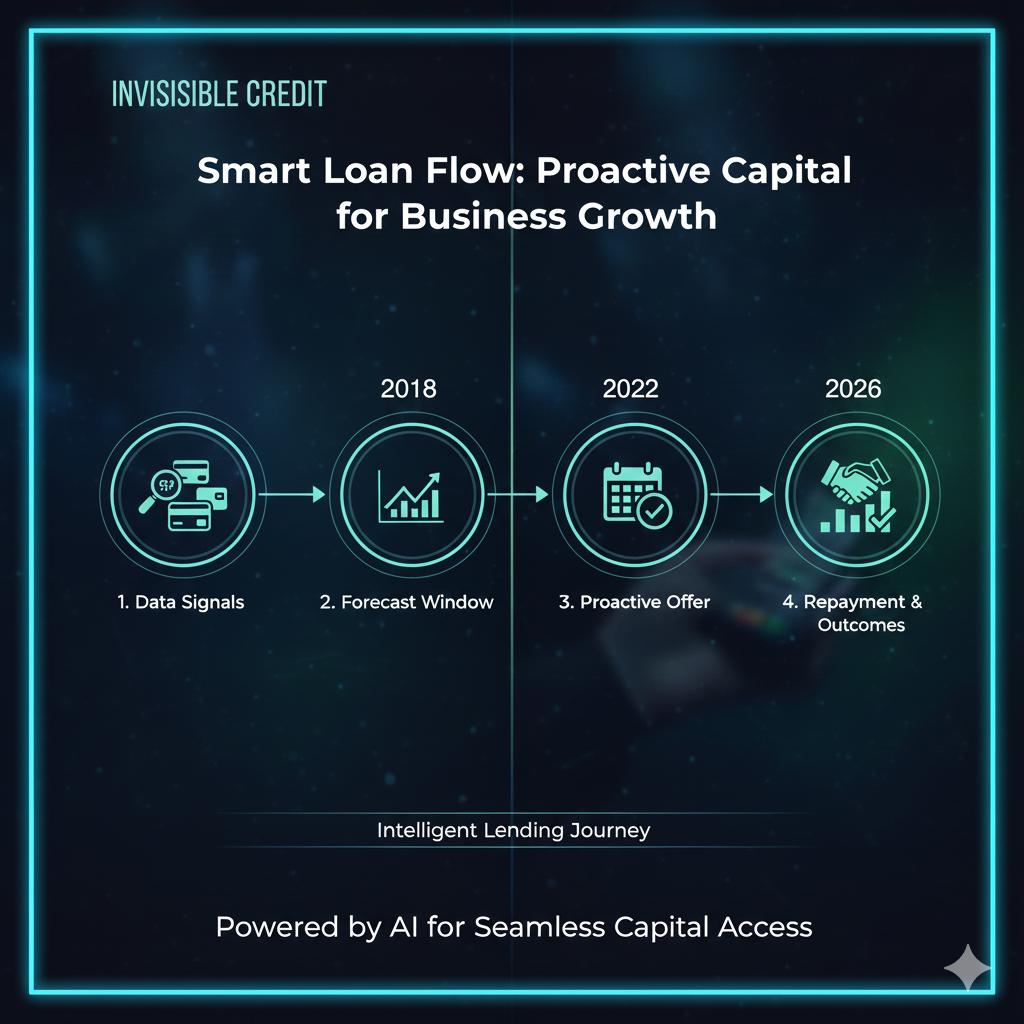

Step one: forecasting your cash timeline

The core idea is a cash timeline.

A system estimates what money will come in, and when. It also estimates what money will go out, and when. Then it calculates risk windows.

If a tight window appears, the system flags a likely need for capital.

That is the first “smart” moment.

Additionally, business lending models often do the same with receivables and payables. A late-paying customer can trigger a stress signal. So can a seasonal expense spike.

Step two: estimating your acceptance probability

Many smart-loan systems also predict something else: whether you will accept.

This is a critical detail. It moves lending closer to marketing.

The model may choose timing, wording, and channel. It may decide to offer a smaller loan with a higher chance of acceptance. It may choose a bigger offer when confidence is high.

Consequently, the offer is not only about your needs. It is also about platform optimization.

This is where ethics becomes urgent.

Step three: dynamic pricing and dynamic limits

In older lending, pricing was mostly static.

In smarter lending, pricing and limits can adjust. They can adjust with new data. They can adjust with new risk signals. They can adjust with macro conditions.

That flexibility can be profitable for lenders. It can also be dangerous for borrowers if it becomes confusing.

Therefore, transparency becomes vital. Clear APR. Clear fees. Clear total repayment. Clear hardship options.

Smart loans can be genuinely beneficial

This is not a doom story. There are real upsides.

Fewer emergencies, fewer humiliating denials

A proactive offer can prevent a crisis.

A small buffer loan can stop late rent. It can stop utility shutoff. It can prevent overdraft spirals. It can keep a business from missing payroll.

That is a proven benefit when offers are fair and repayment is manageable.

Additionally, proactive offers can reduce the emotional pain of applying. Many people avoid loans because of shame or fear. A pre-qualified offer can feel reassuring.

Better inclusion through cash flow insight

Smart lending can help thin-file borrowers.

If a borrower has limited credit history but stable income deposits and responsible spending patterns, cash flow signals can support a confident approval.

Experian and Plaid announced a partnership in June 2025 that aims to use permissioned data to help lenders assess risk more accurately and expand access to credit. (Experian)

Consequently, smart loans can open doors. That is a powerful promise.

Faster working capital for small businesses

Small businesses often do not have time.

A restaurant cannot wait weeks for financing. A merchant cannot miss a holiday inventory cycle. A contractor cannot pause a job because a customer is late.

Cash-flow-based underwriting research has highlighted how bank-statement variables can improve small business underwriting when used responsibly. (FinRegLab)

That is the rewarding side of proactive credit. It supports growth. It supports momentum.

The hidden risks are serious

Smart loans can feel comforting. That is exactly why they can be risky.

The temptation problem: AI offers arrive at weak moments

If a system predicts you will be stressed soon, it can deliver an offer right before that stress hits.

That can be helpful. It can also be manipulative.

A borrower may accept without reflection. A borrower may stack debt. A borrower may use a loan to cover overspending, not a true need.

Consequently, smart loans can turn into smart traps.

Privacy: prediction requires intimate signals

Cash flow prediction can expose personal life patterns.

It can reveal health-related spending. It can reveal family support payments. It can reveal sudden hardship. It can reveal habits.

Therefore, consent must be meaningful. Data collection must be minimal. Storage must be limited. Security must be strong.

Open finance frameworks emphasize safeguards because the data is sensitive and the consequences are real. (World Bank)

Fairness: models can create invisible discrimination

More data does not guarantee fairness.

Models can learn patterns that correlate with protected traits, even if those traits are not collected. A model can penalize people for living in certain areas, shopping in certain stores, or having volatile income.

Additionally, automated systems can make denial feel cold and final.

This is why explainability and fairness testing are critical. Regulators and international bodies have been discussing explainability and model risk concerns around complex AI. (Bank for International Settlements)

Model risk: even lenders fear AI mistakes

A striking 2025 signal is that some lenders are reportedly seeking insurance against AI screening errors in mortgage lending. (Financial Times)

That detail is revealing. It shows confidence and fear at the same time.

AI can reduce cost. AI can increase speed. Yet AI can also misjudge. A misjudge at scale is a disaster.

Therefore, model governance is not optional. It is essential.

What “responsible smart lending” looks like

If smart loans are going to expand in 2026, the industry needs guardrails that feel authentic, not cosmetic.

Predict need, but also predict harm

A mature system does not only predict default risk.

It also predicts borrower harm risk. It estimates whether repayment will create distress. It flags patterns that signal vulnerability.

Consequently, it can reduce limits or slow offers when risk to the borrower is high.

That is a certified sign of responsible design.

Build friction on purpose

Friction sounds bad. Sometimes it is vital.

A short pause. A clear summary. A simple “total cost” screen. A repayment stress check. These moments protect borrowers.

Additionally, the best systems limit repeat borrowing. They watch stacking. They block “loan loops.”

That creates trust. It also protects long-term profitability.

Explain decisions in plain language

If a system approves, explain why. If a system denies, explain why.

Offer a path to improve. Offer a dispute path for wrong data. Offer human support when needed.

GenAI may help lenders communicate better, but it must not become a fake empathy mask. It must stay accurate and verifiable. (McKinsey & Company)

Smart loans in practice: where you see them in 2025

You may already be in the smart-loan world.

Banking apps: pre-approved lines and proactive refinancing

Banks have long offered pre-approved credit. The difference now is timing and personalization.

With better data and models, offers can align with real cash windows. They can also update faster.

However, this also means the “offer pressure” can increase. The most responsible banks will focus on clarity and suitability.

Payroll and earned wage access: the paycheck prediction zone

Payroll-linked products sit close to the most emotional moment in personal finance: payday.

If a system sees your bills landing before your payday, it may offer a small loan or advance. That can be immediate relief.

Still, these offers must be fair. Fees must be clear. Repeat use must be monitored. Otherwise, it becomes a cycle.

Merchant platforms: working capital as a dashboard feature

Marketplaces and payment processors can predict merchant needs with frightening accuracy.

They can see sales volume. They can see seasonality. They can see refund rates. They can see ad spend. They can see chargebacks.

Consequently, they can offer capital before the merchant asks.

This can be profitable and powerful. It can also create platform dependence. A merchant may feel trapped inside one ecosystem.

Video briefings

What changes in 2026

2026 is likely to accelerate smart loans, but with sharper scrutiny.

Agentic AI and “always-on” credit

GenAI is evolving. Workflows are becoming more agent-like.

In 2026, many lenders will try systems that do more than score. They will monitor portfolios. They will propose restructures. They will recommend actions.

This can be a breakthrough in customer support. It can also be a surveillance risk.

Consequently, consent and boundaries will be a major battlefield.

Real-time payments and instant funding

Real-time rails keep expanding globally.

When funding becomes instant, proactive credit becomes more potent. The offer can be accepted and funded in minutes.

That feels thrilling. It also increases impulsive borrowing risk. Therefore, strong “offer clarity” design becomes more vital.

Tougher expectations on model risk

Model risk standards are tightening. Explainability demands are growing.

Regulatory and standard-setting discussions increasingly emphasize governance, validation, and transparency for AI models in finance. (Bank for International Settlements)

Additionally, if lenders are insuring against AI mistakes, that signals a market demand for measurable controls. (Financial Times)

So 2026 may be the year where smart loans must prove they are not just clever, but also safe.

A more honest debate about manipulation

The most uncomfortable topic will become mainstream.

If AI can predict vulnerability, it can time offers to exploit it. That is a harsh truth.

Therefore, regulators and consumer advocates will likely push harder on suitability, affordability checks, and marketing practices.

The winning lenders will treat this as a trust opportunity, not a compliance burden.

How to protect yourself and still benefit

Smart loans are not automatically good or bad. Your habits matter.

Use one simple rule: never borrow in a rush

Even if the offer is instant, you do not have to be.

Pause. Read total repayment. Check fees. Check autopay dates. Confirm the lender identity. Confirm whether the offer is a loan or a credit line.

Additionally, ask one vital question: “What problem does this solve, exactly?”

If the answer is vague, the risk is high.

Keep your obligations visible

Smart loans become dangerous when debt is scattered.

Track active plans. Track payment dates. Track total monthly burden. Reduce stacking.

This is not glamorous. It is proven. It is powerful. It keeps you in control.

Be strict with data permissions

Only grant access when it is necessary.

Prefer reputable providers. Prefer limited access scopes. Avoid products that demand excessive permissions for small credit.

Consequently, you protect your privacy while still using modern credit tools.

Conclusion

Smart loans are reshaping credit in 2025.

AI can forecast your need for capital before you feel it. That can be rewarding, profitable for lenders, and genuinely supportive for borrowers. It can also be risky, invasive, and manipulative if design is careless.

The decisive issue is trust.

In 2026, smart lending will likely grow faster. It will also face stronger model risk expectations and louder fairness debates. Systems will need clear consent, clear explanations, and real protections. Not performative protections. Real ones.

If the industry gets this right, proactive credit can reduce emergencies and expand access. If the industry gets it wrong, “smart loans” become “smart pressure,” and borrowers pay the price.

The future of lending is predictive. The future of good lending is responsible.

Sources and References

- Experian: Experian and Plaid team up to unlock smarter credit decisions (Jun 2025)

- American Banker: How Experian scores thin-file borrowers with cash-flow data (Jun 2025)

- FinRegLab: Sharpening the Focus on Cash-Flow Data for Small Business Underwriting (Jun 2025 PDF)

- FinRegLab: Advancing the Credit Ecosystem with ML and Cash-Flow Data (Jul 2025 PDF)

- World Bank: The Use of Alternative Data in Credit Risk Assessment (PDF)

- McKinsey: Embracing generative AI in credit risk (Jul 2024)

- McKinsey: Banking on gen AI in the credit business (Jul 2025)

- BIS FSI: Paper on AI explainability and model risk (2025 PDF)

- Financial Times: US mortgage lenders insure against AI screening errors (Dec 2025)

- Financial Times: Private credit firms pile into consumer debt (Dec 2025)

- YouTube: AWS re:Invent 2025, reinventing credit origination

- YouTube: Plaid Effects 2025, cash flow data update for lending